Finance for Non-Finance Professionals Training

in Technical TrainingsAbout this training

Master Finance for Non-Finance Professionals: Essential Financial Insights for Better Decision-Making | TheSkope

About This Training

Understanding finance is a key to making well-informed decisions in any role within an organization. This Finance for Non-Finance Professionals training is designed to equip you with essential financial knowledge and tools, even if you don’t have a background in finance. The course will cover fundamental financial concepts and provide practical techniques that you can immediately apply to your professional work, improving your ability to contribute to your organization’s financial decision-making processes.

Why Choose Our Finance for Non-Finance Course?

Our course offers an in-depth introduction to the financial concepts that matter most to non-financial professionals. Each module is designed to simplify complex financial information, allowing you to understand and use finance as a tool for better strategic and operational decisions.

Once you complete this training, you’ll feel confident interpreting financial statements, budgeting, managing costs, and using financial data for smarter business decisions.

Course Highlights

In-Depth Modules: Each module breaks down a key financial concept with clear explanations, practical examples, and real-world applications.

Expert Instructors: Learn from industry experts with years of experience in financial management, budgeting, and strategic decision-making.

Interactive Learning: Reinforce your learning with practical quizzes, real-life case studies, and exercises designed to enhance your understanding of financial principles.

Flexible Access: Study at your own pace with 24/7 access to all course materials, ensuring flexibility for your schedule.

In-Depth Modules: Each module breaks down a key financial concept with clear explanations, practical examples, and real-world applications.

Expert Instructors: Learn from industry experts with years of experience in financial management, budgeting, and strategic decision-making.

Interactive Learning: Reinforce your learning with practical quizzes, real-life case studies, and exercises designed to enhance your understanding of financial principles.

Flexible Access: Study at your own pace with 24/7 access to all course materials, ensuring flexibility for your schedule.

Who Should Enroll?

Business Managers

Project Managers

Marketing and Sales Professionals

Human Resources Professionals

Entrepreneurs and Business Owners

Operations Managers

Anyone looking to understand financial concepts for better decision-making

Business Managers

Project Managers

Marketing and Sales Professionals

Human Resources Professionals

Entrepreneurs and Business Owners

Operations Managers

Anyone looking to understand financial concepts for better decision-making

Why You Should Learn Finance for Non-Finance Professionals?

Improved Decision-Making: Learn how to apply financial concepts in everyday decision-making processes, driving better business outcomes.

Cost Control & Budgeting: Understand the financial aspects of budgeting, cost control, and resource allocation to ensure financial efficiency.

Career Advancement: Expand your professional skills with financial literacy that enhances your value within any organization.

Strategic Financial Planning: Learn to interpret financial data and contribute to long-term strategic planning and growth.

Increased Organizational Efficiency: Implement financial tools to streamline operations and improve profitability.

Improved Decision-Making: Learn how to apply financial concepts in everyday decision-making processes, driving better business outcomes.

Cost Control & Budgeting: Understand the financial aspects of budgeting, cost control, and resource allocation to ensure financial efficiency.

Career Advancement: Expand your professional skills with financial literacy that enhances your value within any organization.

Strategic Financial Planning: Learn to interpret financial data and contribute to long-term strategic planning and growth.

Increased Organizational Efficiency: Implement financial tools to streamline operations and improve profitability.

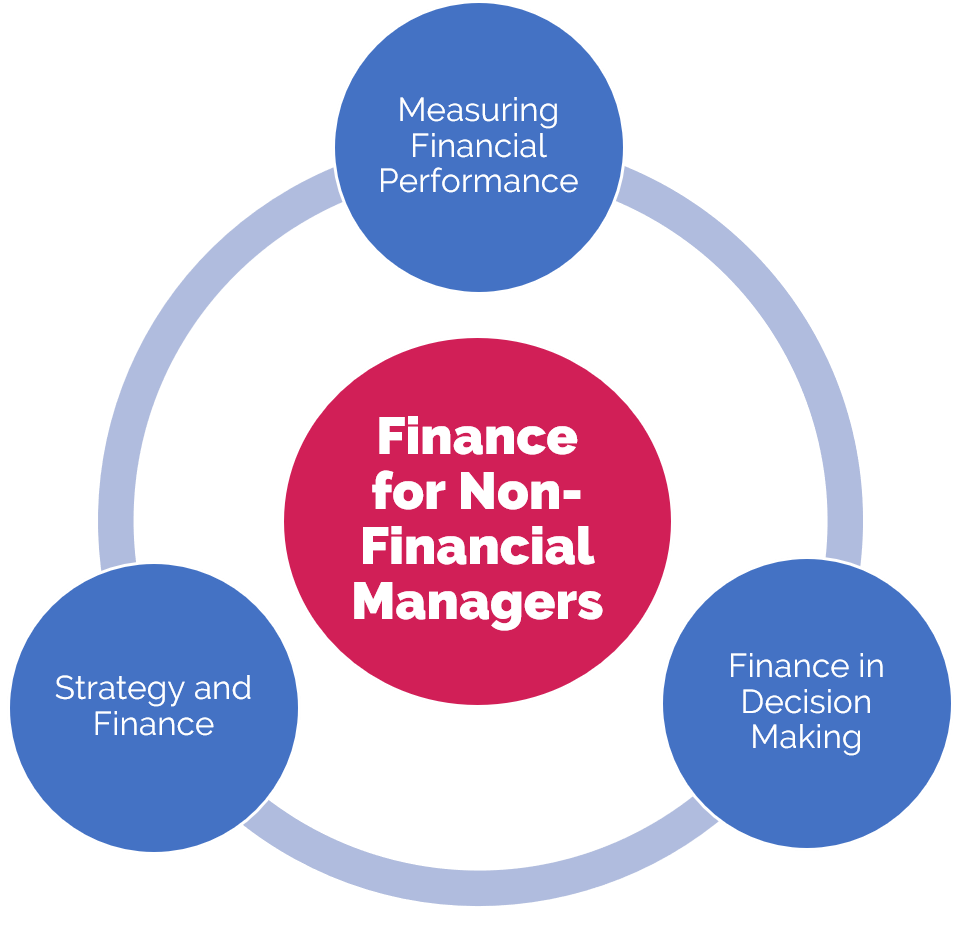

Finance for Non-Finance Professionals Course Structure

Introduction to Finance for Non-Finance Professionals: Understand basic financial concepts and their importance in everyday business functions.

Understanding Financial Statements: Learn how to read and interpret balance sheets, income statements, and cash flow statements.

Budgeting & Forecasting: Master the techniques for budgeting, forecasting financial outcomes, and analyzing variances.

Cost Management & Profitability: Learn about cost types, cost allocation, and profitability analysis to make informed decisions.

Financial Ratios & Key Metrics: Understand how to analyze and interpret financial ratios like profitability, liquidity, and efficiency to evaluate a company’s performance.

Real-World Case Studies: Study examples from various industries to see how financial knowledge supports effective decision-making.

Interactive Assignments and Projects: Engage in hands-on projects that simulate real financial situations, ensuring you gain practical experience.

Final Assessment and Certification: Complete a final assessment to test your knowledge and earn a certificate of completion.

Introduction to Finance for Non-Finance Professionals: Understand basic financial concepts and their importance in everyday business functions.

Understanding Financial Statements: Learn how to read and interpret balance sheets, income statements, and cash flow statements.

Budgeting & Forecasting: Master the techniques for budgeting, forecasting financial outcomes, and analyzing variances.

Cost Management & Profitability: Learn about cost types, cost allocation, and profitability analysis to make informed decisions.

Financial Ratios & Key Metrics: Understand how to analyze and interpret financial ratios like profitability, liquidity, and efficiency to evaluate a company’s performance.

Real-World Case Studies: Study examples from various industries to see how financial knowledge supports effective decision-making.

Interactive Assignments and Projects: Engage in hands-on projects that simulate real financial situations, ensuring you gain practical experience.

Final Assessment and Certification: Complete a final assessment to test your knowledge and earn a certificate of completion.

Testimonials

"This course made finance easy to understand and apply. The content was simple yet effective, and the case studies were extremely insightful."

— Priya Sharma, Marketing Manager ⭐⭐⭐⭐⭐

"I didn’t think I would be able to understand finance, but this course changed that. The trainers were very knowledgeable and helped me grasp key concepts in no time."

— Arvind Patel, Operations Manager ⭐⭐⭐⭐⭐

— Priya Sharma, Marketing Manager ⭐⭐⭐⭐⭐

— Arvind Patel, Operations Manager ⭐⭐⭐⭐⭐

Enroll Today

Join professionals across industries who have transformed their decision-making processes with our Finance for Non-Finance Professionals course.

Sign up today and start your journey toward financial literacy!

Sign up today and start your journey toward financial literacy!

Certification Exam

Candidates will complete an online exam with multiple-choice questions. A passing score of 60% is required to earn your certificate of completion.

A hard copy of your certificate is available for an additional fee of ₹100.

A hard copy of your certificate is available for an additional fee of ₹100.